What are the prior authorizations required to launch a fintech in Francophone Africa?

What authorizations are required before starting operations? What steps need to be taken? Are you an entrepreneur in Francophone Africa looking to launch a fintech, mobile money service, neobank, crypto platform, or crowdfunding platform? We answer your questions.

Are you an entrepreneur in Francophone Africa? Do you want to launch a fintech but don't know where to start? Do you know that some fintechs are subject to prior authorizations but aren't sure whether this applies to you?

If this sounds like you, you've come to the right place! In this article, we aim to give you some guidance to help you navigate this complex regulatory landscape.

First and foremost, it is important to understand that the rules will vary entirely depending on the activity you wish to develop.

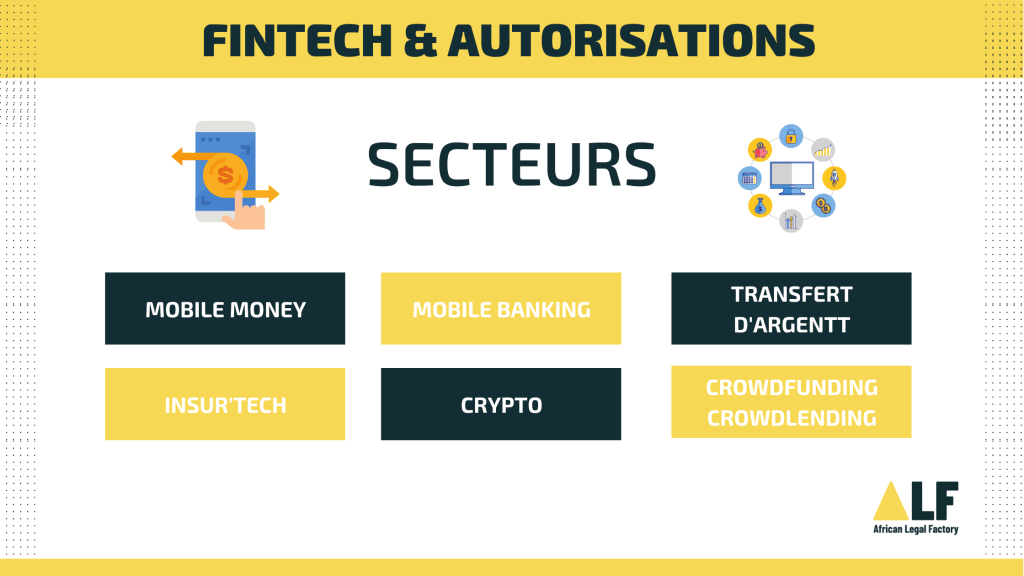

In this article, we cover the regulatory framework applicable to launching an activity in:

- E-money issuance and distribution, Mobile Money;

- Mobile Banking, deposits and withdrawals;

- Rapid money transfer;

- InsurTech activities;

- Crypto-asset provision and management; and

- Crowdfunding and Crowdlending.

1. E-money issuance and distribution, Mobile Money

First, it should be noted that this activity is formally regulated by the regulatory and supervisory authorities of Francophone African countries, particularly within the West African Monetary Union (WAMU/UMOA), the Economic and Monetary Community of Central Africa (CEMAC), as well as in Burundi, the Comoros, Djibouti, and Madagascar.

What license is generally required to issue e-money?

To issue and distribute e-money, fintechs must independently apply for an individual license as an e-money institution from the regulatory authority — generally the central bank and/or any other authority specified in the applicable regulations.

To obtain this license as an e-money institution, the following essential requirements must be met — which may be strengthened depending on the jurisdiction:

- the legal incorporation of the entity as a public limited company (SA), a multi-shareholder limited liability company (SARL), a mutual, a cooperative, or an economic interest group;

- the establishment of the registered office in the target jurisdiction and the exclusive limitation of the corporate purpose to e-money issuance;

- provision of a minimum share capital meeting regulatory thresholds (e.g., 300 million CFA francs in the UMOA zone);

- the immediate segregation of funds representing the counterpart of e-money in a dedicated bank account exclusively reserved for this purpose in the target jurisdiction;

- provision of draft contract(s) for opening escrow account(s) for funds received in exchange for e-money in circulation;

- provision of a draft service agreement for customers and implementation of a complaints management system for customers and relevant stakeholders;

- provision of business forecasts and financial projections covering at least three (3) years of activity, based on pessimistic, moderate, and optimistic sensitivity assumptions;

- compliance with regulatory requirements relating to technical specifications for e-money issuance solutions to: (i) ensure high platform availability, (ii) preserve message integrity, (iii) maintain information confidentiality, (iv) guarantee transaction authenticity, and (v) ensure transaction non-repudiation;

- implementation of a proven business continuity framework;

- implementation of a risk management strategy;

- adoption of technical and operational measures to facilitate interoperability with other payment systems;

- provision of evidence of an audit trail enabling full traceability of transactions from the origin of the payment order to its settlement;

- compliance of the licensing file with the templates and procedures defined by the central banks.

It is very difficult for a startup to meet all of these requirements from the outset. For this reason, in order to operate in this space, fintechs generally need to establish partnerships — acting as technical operators — with licensed issuing institutions (banking institutions, payment institutions, and microfinance institutions) in their capacity as issuers and distributors of e-money.

To act as a technical operator, a partnership agreement must be concluded with a licensed issuing institution. This collaboration must be limited to the technical processing of e-money or its distribution, under the issuer's responsibility. In this case, any public-facing communications by the technical partner must identify the issuing institution. The responsibility for e-money issuance cannot be outsourced to a technical operator.

Are there additional obligations for payment institutions when launching a new product?

At the regulatory level, banks and payment institutions are generally required to notify the Central Bank prior to commencing their e-money issuance activities or launching any new e-money-related service to the general public. This notice period is, for example, two months within the UMOA zone.

This allows regulatory authorities sufficient time to assess the compliance of the services to be deployed and to issue recommendations.

The information file for a new product launch must include, in particular:

- a detailed project presentation note;

- the customer complaints management procedures;

- measures taken to comply with anti-money laundering and counter-terrorism financing (AML/CFT) requirements;

- a document describing the stakeholders involved;

- the operational processes of the product or service offered;

- a risk mapping and the precautionary measures associated with the use of the product or service;

- a draft usage agreement for the product(s) or service(s) offered;

- any other draft partnership agreement referenced in the file, setting out, among other things, the pricing schedule for the proposed services.

2. Mobile Banking, deposits, withdrawals

The following activities in Francophone Africa generally require a formal banking license application to be submitted to the relevant regulatory and supervisory authorities:

- digital banking (neobank),

- online banking (a traditional institution undergoing partial digital transformation),

- savings collection and withdrawal activities.

Looking for legal assistance for your fintech?

If you would like support in structuring your fintech (company formation, licensing, compliance, fundraising), fill in this questionnaire and we will get back to you promptly.

3. Rapid money transfer

The rapid money transfer activity falls, in most Francophone African countries, under the regulations applicable to the management and provision of payment instruments and/or the collection of public funds.

In this regard, fintechs wishing to carry out these operations generally need to apply for a banking license as an authorized service provider.

In the absence of such a license, fintechs may work with licensed institutions as agents. However, this agency relationship must be approved by the supervisory authorities (the Central Bank and/or government bodies acting as oversight bodies).

4. Insurance "InsurTech"

This sector is characterized by the absence of a specific regulatory and legal framework for digital innovation in insurance operations — this remains the case in the vast majority of Francophone African countries to date. However, several regulators have begun working on the subject. Among the initiatives identified, ongoing work is noted at the level of the Inter-African Conference on Insurance Markets (CIMA), aimed at developing a regulation on electronic insurance.

Given this regulatory reality, fintechs and startups operating in Francophone Africa should comply with the traditional insurance regulations and Insurance Codes currently in force in order to apply for an operating license. In addition, they should also be prepared to justify to the regulator the value of their 100% digital business model and its capacity to innovate the insurance product offering.

5. Crypto-asset provision and management

Cryptocurrencies are currently the subject of in-depth reflection among regulators across Francophone Africa. Regulators are increasingly raising awareness among economic actors about the potential risks associated with the use of cryptocurrencies. As a result, crypto-asset management falls outside the current regulatory framework, unlike formal banking activities such as credit or payment services.

Consequently, it is strongly recommended that cryptocurrency players formally seek the opinion of the relevant regulatory and supervisory authorities on their projects, business models, and products, in order to avoid potential sanctions for conducting illegal activities or for risks of money laundering and terrorism financing.

6. Crowdfunding and Crowdlending

The absence of specific regulations on participatory financing does not favor the widespread development of this activity in Francophone Africa. However, discussions are well advanced at the level of banking and capital market regulators, with a view to proposing an appropriate legal framework. Some countries, such as Morocco and Tunisia, have already made significant progress on this front.

In any case, at this stage it is recommended that promoters of participatory financing or crowdfunding platforms in Francophone Africa approach the relevant regulatory and supervisory authorities to seek a formal opinion and authorization (Central Bank and/or government bodies acting as oversight bodies).

By way of conclusion, the regulatory framework applicable to fintechs is still being developed and is expected to undergo significant changes in the near future. The descriptions above are intended only to provide an overview of the rules most broadly applicable in West Africa. It is imperative to verify, for each target country, the applicable national and regional regulations.

🔜 Once established, the fintech is subject to regulatory obligations regarding cybersecurity, personal data protection, and anti-money laundering compliance. For more information on these topics, please refer to this article.

🚨 The information listed above does not constitute legal advice. To obtain a legal opinion on your specific situation or project, we recommend consulting a lawyer.

Ready to launch your fintech in Francophone Africa?

Whether you are launching a mobile money service, neobank, money transfer platform, insurtech, crypto venture, or crowdfunding platform, our lawyers can support you with legal structuring and licensing procedures. Fill in this questionnaire and we will get back to you promptly.